香港中环雪厂街二号圣佐治大厦五楼503室

香港中环雪厂街二号圣佐治大厦五楼503室 +852 2868 0696

+852 2868 0696

Family Offices in Hong Kong: Tax Concessions, Re-domiciliation, and Proposed 2026 Reform

7 Jul 2026

Hong Kong stands out as a premier destination for family offices, offering a unique blend of business-friendly policies, robust legal frameworks, and strategic advantages.

1. Business-Friendly Tax Regime

Hong Kong imposes low and simple taxes with no VAT, capital gains, dividend, or inheritance taxes. As at June 2026, Hong Kong holds 58 comprehensive avoidance of double taxation agreements, with another 16 under negotiation.

2. Robust Legal System

The city operates under a Common Law framework, providing strong rule of law and investor protection.

3. World-Class Financial Services

As a leading global hub for private banking, asset management and professional advisory services, Hong Kong offers tailored solutions for HNWIs and families.

4. Skilled Talent Pool

Hong Kong is home to a highly skilled, multilingual workforce.

5. Government Support

The Hong Kong government actively supports family offices through initiatives like FamilyOfficeHK under InvestHK and tax concessions for single-family offices.

6. Strategic Location

Hong Kong serves as a gateway to Mainland China and the Asia-Pacific region.

Re-Domiciliation of Family Offices

As of May 2025, non-Hong Kong incorporated companies, including family offices, can re-domicile to Hong Kong under a new statutory regime. This allows family offices to relocate their operations while retaining their legal identity and continuity. The streamlined process involves an application to the Companies Registry, with approvals typically granted within two weeks.

Key highlights:

- The family office retains all assets, rights, obligations, and legal standing post-transfer

- The family office obtains the same rights as family offices incorporated in Hong Kong

- A fixed application fee (HK$6,050 electronically / HK$6,725 in hard copy)

- Upon approval, the family office becomes a Hong Kong-incorporated entity and must deregister in its original jurisdiction within 120 days

Regulatory and tax implications:

- Tax continuity is preserved – profits tax applies only to income sourced in Hong Kong

- Relief and credits are available to avoid double taxation during transition

- No stamp duty is triggered by re-domiciliation

Tax Concessions for Family-owned Investment Holding Vehicles (FIHVs)

Hong Kong’s Inland Revenue (Amendment) (Tax Concessions for Family-owned Investment Holding Vehicles) Ordinance 2023 introduced a 0% profits tax concession for qualifying FIHVs.

Who qualifies:

- ≥ 95% beneficial interest held, in aggregate, by one or more than one member of the family (charities ≤ 25%, outsiders ≤ 5%)

- Normally managed and controlled in Hong Kong, outsourcing is permissible

- Holds ≥ HK$240 million specified assets (shares, stocks, bonds, debentures, etc.)

- Carries on all core income-generating activities in Hong Kong with ≥ 2 qualified full-time staff and ≥ HK$2 million local operating spend

- Not a business undertaking

What’s covered:

- Transaction in specified assets (qualifying transactions): trading securities, FX, private-company shares, derivatives, etc.

- Transactions incidental to the carrying out of qualifying transactions (receipts capped at 5% of total receipts)

Practical steps to obtain tax certainty:

- Map ownership to confirm ≥ 95% family control (with any charity/unrelated shareholding within limits).

- Elect for the concession – once, in writing – before filing the first relevant tax return.

- Verify substance annually: head-count, spend, and asset NAV.

- Monitor transactions for the 5% incidental threshold and private-company anti-avoidance triggers.

- Maintain documentation (family tree, group chart, management agreements, NAV calculations) ready for audit or advance-ruling submission.

Legislative Update: 2026 Preferential Tax Regimes Bill

- On 12 June 2026, Hong Kong gazetted the Inland Revenue (Amendment) (Preferential Tax Regimes for Funds, Family-owned Investment Holding Vehicles and Carried Interest) Bill 2026.

- The Bill proposes to expand Hong Kong’s preferential tax regimes for:

- funds;

- Family-owned Investment Holding Vehicles;

- carried interest.

- Expanded qualifying asset classes

- The 0% profits tax concession would be expanded to cover additional asset classes, including:

- digital assets;

- gold and other precious metals;

- specified commodities;

- carbon credits;

- private credit.

- The 0% profits tax concession would be expanded to cover additional asset classes, including:

- Broader eligible fund structures

- Eligibility would be extended beyond traditional open-ended fund structures to include:

- certain “fund-of-one” structures;

- wholly-owned investment vehicles;

- pension funds;

- charity funds.

- Eligibility would be extended beyond traditional open-ended fund structures to include:

- Carried interest tax relief

- The Bill would enhance tax relief for performance-linked returns, including carried interest, for private equity and venture capital funds.

- This is intended to strengthen Hong Kong’s competitiveness as a private capital and asset management hub.

- Removal of 5% incidental threshold

- The existing draft memo states that the concession covers transactions in specified assets and that receipts from incidental transactions are capped at 5% of total receipts.

- The Bill proposes to remove this 5% incidental threshold, giving family offices greater flexibility in treasury, cash management and interest-earning activities.

- Interaction with non-tax incentives

- Hong Kong’s Capital Investment Entrant Scheme provides a residency pathway for individuals making a qualifying HK$30 million investment, including at least HK$3 million into a government-managed investment portfolio.

- The scheme may also allow family members to be included, facilitating relocation alongside the family office structure.

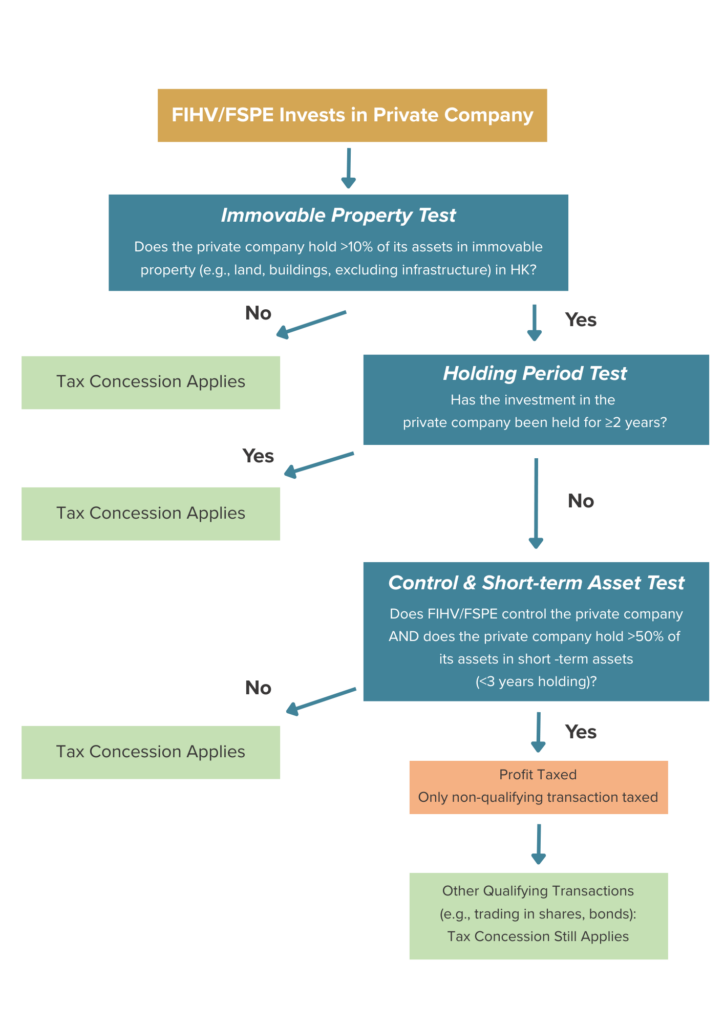

Anti-Avoidance Measures

Hong Kong has implemented anti-avoidance measures to ensure that tax concessions are not abused. These measures include tests for immovable property, holding periods, and control and short-term asset tests.

With its favourable tax regime, robust legal system, world-class financial services, skilled talent pool, and strong government support, Hong Kong is the ideal location for family office. Whether you are looking to establish a new family office or re-domicile an existing one, Hong Kong offers the perfect environment for long-term wealth planning and growth. Please contact us for further information.

Disclaimer: This article is for reference only. Nothing herein shall be construed as Hong Kong legal advice or any legal advice for that matter to any person. Oldham, Li & Nie shall not be held liable for any loss and/or damage incurred by any person acting as a result of the materials contained in this article.