Suite 503, 5/F, St. George's Building, 2 Ice House Street, Central, Hong Kong

Suite 503, 5/F, St. George's Building, 2 Ice House Street, Central, Hong Kong +852 2868 0696

+852 2868 0696

Are you ready for the implementation of the new tax laws in 2019?

9 Jan 2019

There is no doubt that year 2018 was a busy year for Hong Kong tax advisors with the various new developments in Hong Kong tax laws. Now we are in 2019 – how will these new developments have an impact on you?

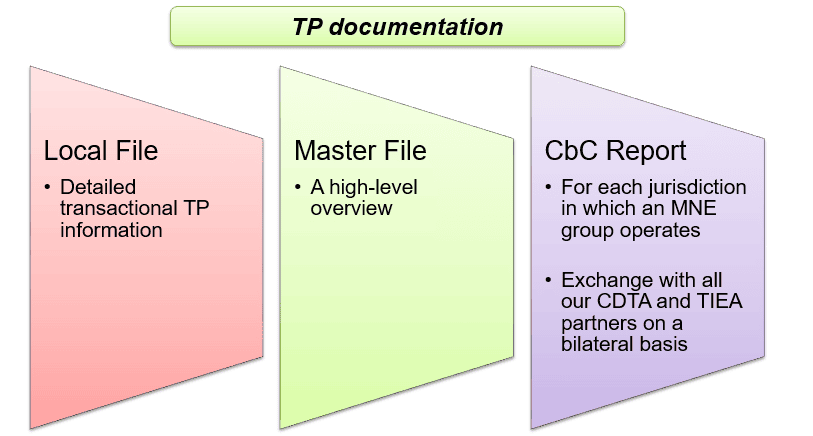

(1) The introduction of the 3-tiered standard transfer pricing documentation for Hong Kong entities engaging in cross-border related-party transactions

Who need to prepare for the reports?

You are likely to subject to reporting if you are an entity with presence in two or more jurisdictions and:-

• Having a total revenue exceeding HK$400 million;

• Having a total assets exceeding HK$300 million;

• Having more than 100 employees;

• Having intra-group related party transaction in one of the following scenarios:-

o transfer of properties (other than financial assets and intangibles): exceeding HK$220 million;

o transaction of financial assets: exceeding HK$110 million;

o transfer of intangibles: exceeding HK$110 million;

o others: (e.g. service income and royalty income): exceeding HK$44 million.

Even if you are subject to Local File and Master File reporting, you may still be exempted from Country-by-Country reporting if your annual consolidated group revenue does not exceed EUR750 million (i.e., approximately HK$6.8 billion).

| Details to be included | Filing due dates | |

| Local File | Detailed transactional transfer pricing information such as details of the transactions, amount involved in the transactions and a transfer pricing analysis. | These filings are required for accounting periods beginning on or after 1 April 2018 and must be prepared within 9 months after the end of each accounting period. |

| Master File | A high-level overview of the group, including documenting the global business operations, transfer pricing policies and global allocation of income. | |

| Country-by-Country Reporting | • To be filed by the ultimate parent entity of a multinational enterprise (“MNE”) in its tax jurisdiction.• Sets out the amounts of revenue, profits and tax paid as well as certain indicators of economic activity such as number of employees, state capital, retained earnings and tangible assets for each jurisdiction in which a MNE operates. | The filing is required for accounting periods beginning on or after 1 January 2018 and must be prepared within 12 months after the end of each accounting period. |

OLN’s observations

Transfer pricing policy requires holistic review of intra-group transaction and group overhead allocation. Aftermath ratification is usually problematic. It is therefore advisable for multinational corporations to carry out preemptive measures as soon as possible. As this is the first piece of legislation in Hong Kong specifically addressing transfer pricing matters with many uncertainties in the application of the law, it is expected that the Hong Kong Inland Revenue Department (“HKIRD”) would provide further guidance in this area through new or revised Departmental Interpretation and Practice Notes. Taxpayers should continue to monitor the developments in order to assess their transfer pricing documentation obligations.

(2) Other key new developments

Lorem initius…

| Key Features | OLN’s observations/ comments | ||

| The implementation of the two-tiered profits tax rates regime | From the year of assessment 2018/2019 onwards (i.e., commencing on or after 1 April 2018), the profits tax rate for the first HK$2 million of profits of corporation will be at 50% of the corporate tax rate of 16.5% (i.e. 8.25%). | Before the implementation of the two-tiered profits tax rates regime, Hong Kong has already provided a 8.25% concessionary profits tax rate to corporates conducting the following activities in order to strengthen Hong Kong’s position as an international asset and wealth management center and drive demand for the related professional services in Hong Kong:- • Qualifying corporate treasury centre; • Qualifying professional reinsurance business; • Authorized captive insurance business; • Qualifying aircraft lessor; • Qualifying aircraft leasing manager. The two-tiered profits tax rates regime aims to reduce the tax burden on enterprises especially small and medium enterprises and startup enterprises. Taxpayer should be aware that in case of connected entities, only one enterprise would be eligible for the two-tiered rates. | |

| Automatic exchange of financial information in tax matters (“AEOI”) | HKIRD has already started conducting AEOI with 50 jurisdictions including Mainland China, United Kingdom, France, Singapore and Japan from September 2018. It means that HKIRD would have the obligation to provide information where requested by tax authorities of these jurisdictions. | Currently Hong Kong has activated AEOI with 50 jurisdictions which would soon extend 25 more jurisdictions including Switzerland, Cayman Islands and Cyprus [1]. Hong Kong plans to expand the list of AEOI jurisdictions to 126 jurisdictions by being one of the participants of the Convention on Mutual Administrative in Tax Matters. United States, British Virgin Islands are 2 of the jurisdictions that have already joined the Convention but not currently one of the AEOI jurisdictions. | |

| Stamp duty on residential properties | To address the overheated property market, the Government has employed rounds of demand-side management tax measures including the followings: • Special Stamp Duty (applying to sellers who sell residential properties within 3 years of purchase); • Buyer’s Stamp Duty (applying to non Hong Kong Permanent Residents); • Doubled ad valorem Stamp Duty (of which Hong Kong Permanent Residents (“HKPR”) who do not own any other residential property in Hong Kong at the time of purchasing a residential property are not affected); the recent tax measure is the New Residential Stamp Duty of which the flat rate of 15% would apply to a HKPR who acquires more than one property under a single instrument, even though that HKPR does not own other residential property at the time of purchase. | Notwithstanding the recent cooling down of the market for residential properties, there is currently no indication from the Government of the possible relaxation of the tax measures. However there is no doubt that the Government would continue to monitor the market for residential properties and would introduce tax measures in response to the market. | |

| Tax measures in response to the population ageing | The Government has continuously introduced tax measures in response to the population ageing including the following:- • Starting from 1 April 2019, taxpayers can claim deductions for purchasing eligible health insurance products for themselves or their specified relatives[2] under the Voluntary Health Scheme up to HK$8,000 per insured person; • The Inland Revenue and MPF Schemes Legislation (Tax Deductions for Annuity Premiums and MPF Voluntary Contributions) (Amendment) Bill 2018 has been introduced to seek to introduce tax deductions for deferred annuity premiums and Mandatory Provident Fund Tax Deductible with the maximum tax deductible limit for a taxpayer to be HK$60,000 per year. | It is expected that the Government would continue to introduce tax measures to alleviate the long-term pressure on the public healthcare system and to encourage savings for the retirement. | |

| Continuous expansion of the treaty network | Hong Kong has recently signed a Comprehensive Double Taxation Agreement (“CDTA”) with Finland which is the 40th CDTA signed by Hong Kong and the first one signed with a Nordic country. | Hong Kong has continuously expanding the treaty network to bring a greater degree of certainty on taxation liabilities for those who engage in cross-border business activities and help promote bilateral trade and investment activities. There are currently 13 CDTA negotiation in progress, including Germany and Macao SAR. |

Taxpayers should continue to monitor the development in the various areas of tax laws and take appropriate steps to manage the tax risks.

OLN provides a full range of tax advisory services. If you have any questions regarding the above or on any tax issues, please contact one of the members of the tax advisory team.

[1] On the basis of bilateral competent authority agreements or a multilateral competent authority agreement under the Convention on Mutual Administrative Assistance in Tax Matters.

[2] The taxpayer’s spouse and children, and the taxpayer’s or his/her spouse’s grandparents, parents and siblings.

Author(s)

Recent News