Suite 503, 5/F, St. George's Building, 2 Ice House Street, Central, Hong Kong

Suite 503, 5/F, St. George's Building, 2 Ice House Street, Central, Hong Kong +852 2868 0696

+852 2868 0696

Nip conflicts in the bud

14 Aug 2019

因為家族企業糾紛將家族成員告上法庭是一件令人遺憾,卻也不是不常見的事。我們當然不樂於看見家族的和諧受到破壞,但怎樣才能防患於未然?在本文中,我們將探討如何利用企業管治工具協助家族企業傳承的規劃。

從範例中學習

你可能還記得,身為香港第二大地產發展商和上市公司新鴻基地產有限公司(新鴻基)董事局成員的郭氏兄弟,曾透過訴諸法律程序解決公司控制權爭議的事。2008年,大哥郭炳湘向香港法院申請禁制令,以圖阻止董事局終止其被任命為董事局主席兼行政總裁,及/或改任他為非執行董事。該禁制令最終遭到撤銷,理由是法院不能干預涉及公司內部管理事宜的董事局事務。

雖然新鴻基的範例涉及董事局層面的事宜,但郭炳湘提起的法律行動反映了少數股東的困難。在現行法律框架「少數服從多數」的原則下,一般而言,法院不能協助少數股東維持其董事職位。

另一個關於家族企業控制的範例為鏞記控股有限公司 (鏞記控股),該公司作為最終控股公司從事經營以燒鵝聞名的鏞記酒家業務。甘健成(原名琨勝)鑑於弟弟甘琨禮不公平地損害他於鏞記控股的利益,因此針對琨禮提出呈請,要求琨禮全面收購他的股份,或者讓鏞記控股清盤。最後,終審法院於2015年作出清盤令,但讓該清盤令暫緩28天生效,以待雙方商討收購的條款(但雙方最後亦未能就此達成協議)。尤其令人遺憾的是,雙方原則上同意了收購安排,但卻無法確定特別是價格等細節。結果,清盤一事無可避免,並交由外部的專業清盤人處理清盤程序。

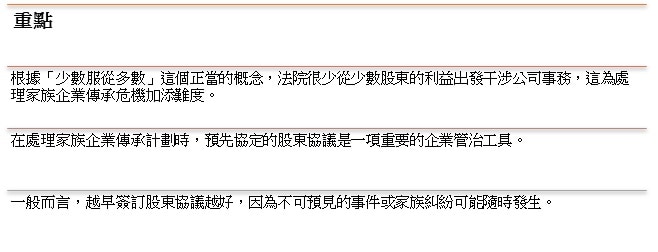

從上述的範例來看,根據「少數服從多數」這個正當的概念,法院很少從少數股東的利益出發干涉公司事務。此外,雖然在現行的框架下有一些可以幫助少數股東的機制,令到他們免受多數股東的壓迫,但這種機制會導致不確定或者激烈的結果,未必能符合少數股東原先的目的,所以光靠這種機制是不足夠的。

這說明要解決家族企業傳承的問題,是需要額外的方法。例如,在鏞記個案中,如果股東事先就股份收購機制在股東協議中達成共識,就可以避免這種結果。股東只需要在股東協議上提前議定如何釐訂股份的收購價,無論是通過淨資產價值(NAV)法,市盈率法還是現金流量法。一旦立訂規則,股東只需要遵循白紙黑字的條款,就可以免於任何不必要的爭論和衝突。

然而,股東協議只是基於企業管治這個更廣泛的概念的一項工具,而企業管治則是任何家族企業傳承計劃中的重要一環。

企業管治工具

企業管治是指公司管理層、董事局、股東和其他持份者之間相互關係的一種規範化。在家族企業的脈絡裏,這些成員還包括既非董事亦非管理層的家族成員。企業管治對公司的順利運營和不同持份者的平衡至關重要。

家族企業的企業管治工具可以包括:

- 《公司條例》(第622章): 第622章載有規管香港公司的條文,以及在香港以外成,但在香港設立營業地點的公司。

- 公司章程 : 公司章程必須在公司註冊處註冊為公開資料,這不利於保障家族隱私,而且不應經常修改。

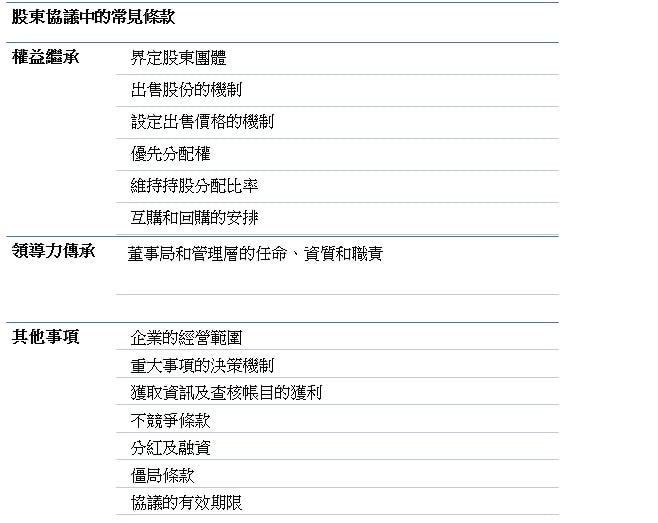

- 股東協議:股東協議通常由所有股東簽署,並且通常具有法律約束力,以便根據預先議定的規則管理公司,並確保股東通過協議去確定其權利和協議牽涉的範圍。

- 獨立董事/外聘顧問:運用獨立董事或外聘顧問可以保障公司的整體利益,但更適合較大型的家族企業。

- 信託營運/家族辦公室: 這更適合已經發展到第二代或第三代的家族企業。

股東協議

毫無疑問股東協議可以解決許多在家族企業傳承過程中出現的企業管治問題。股東協議是公司所有股東之間簽訂的合同,以確定各自的權利和責任,及使公司的管理更有條理。藉着規管股東之間的關係、公司管理和股份擁有權,股東協議發揮了補充公司章程的作用。股東還可以根據股東協議有效利用其股份,或者利用當中的條款以各股東都能接受的方式退出公司。

此外,股東協議的簽訂時機是非常重要的。實際上,人們總會遇到完全無法預見的事,例如死亡、精神上無行為能力、離婚或家庭內的突然危機和爭議。一般而言,越快簽訂股東協議越好,因為不可預見的事件或家庭糾紛可能隨時發生。如果股東協議在早期階段達,當家族成員數目較少時(在家族成員自然橫向增長前),自然可以更容易達成一致的共識。

結語

家族通過合同安排正式化成員之間的關係,這或許不符合傳統中國社會長幼有序的概念而對有些人聽起來有點奇怪。但是,合同條款確實在一定程度上能夠解決家族企業的潛在糾紛。如果你不想看到經營長久的家族企業分崩離析,最好還是防患於未然。

(文章首次在香港特許秘書公會2019年8月號會刊發表 (http://csj.hkics.org.hk),由 Ninehills Media Ltd 出版 。)

Author(s)